First, create a diversified portfolio of different dividend-paying stocks. If your dividends are coming from a single source, you run the risk losing what could be a significant portion of your income should the company decide to discontinue their dividend payments. With a diversified portfolio, your regular dividend income stream could continue, buffered by the on-going payments of the other stocks in your portfolio. Although diversification does not guarantee against the risk of loss in a declining market, it can help to reduce the market volatility risk of your overall portfolio.

Second, when building your dividend-income portfolio, look for high-quality companies in sectors that have historically paid out a steady stream of dividends to shareholders. Finding these stocks can be tricky, but there are a few good places to start. Companies in stable industries or in highly-regulated markets such as electric utilities are typically good candidates for a dividend-income portfolio. These companies usually face fewer threats to their business and fewer interruptions of their cash flow, making it less likely that they would have to discontinue dividend payments.

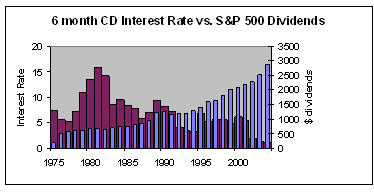

The Dow Dividend Strategy has been a very good way to mechnically select stocks with sustainable dividends, growth in dividends and growth of capital. When you compare what history has shown regarding growth of dividend income vs. the reliability of fixed income investments (chart below) for income over the long run, the asset allocation decision is simple.